What happened?

Singapore REITs have been under pressure in March 2026.

Recently, we have also seen a jump in the 6-month Singapore T-bill yield.

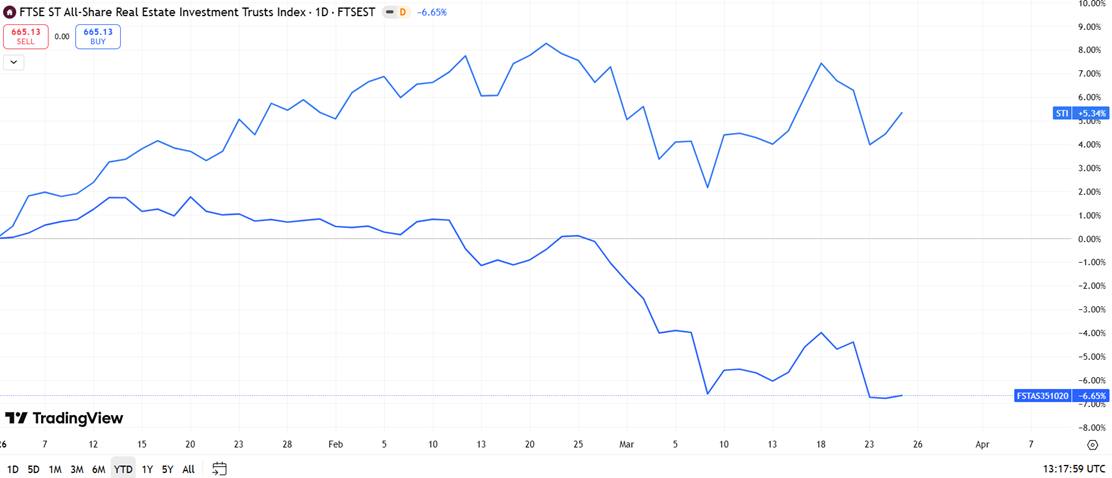

This has led to a 7% decline in an index of Singapore REITs has declined by 7% so far this month, compared to the 2% pullback in the Straits Times Index (STI) (as of 26 March).

With the fall in the share prices of Singapore REITs, I saw a question in the Beansprout Telegram group asking about my thoughts on Singapore REITs.

After all, the correction in the share price of Singapore REITs has also led to more attractive valuations, with some REITs offering a dividend yield of 6% and above.

In this article, we take a deeper look at what the rise in interest rates mean for Singapore REITs, what are the fundamentals of different sectors, and if they are worthwhile buying.

Why are S-REITs falling in March 2026?

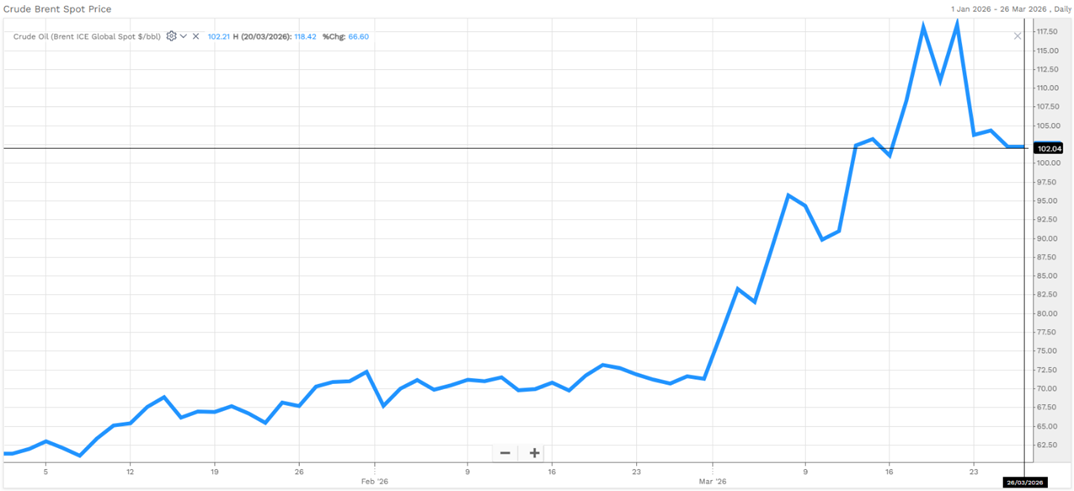

#1 – Oil prices surged above US$110/bbl amid structural supply disruption that could last till 2028.

The closure of Straits of Hormuz has increased concerns about tightening global supply. This is compounded by missile damage to critical LNG infrastructure in Qatar, which could deepen the disruption over a longer period of time.

As oil prices affect the price of goods and services on a broader scale, the fear of prolonged high oil prices drove up inflation expectation.

On 23 March 2026, brent crude soared 58% month-to-date to a high of US$114/bbl .

If oil prices remains elevated for a prolonged period, it will lead to higher inflation. Risk of rising inflation could drive Central Banks to hike interest rates in order to keep their targeted inflation rate.

#2 – Rising U.S. 10-year Treasury bond yield reflects moderation of rate cut expectations

In fact, that was the message from US Federal Reserve at the Fed meeting on 18 March 2026. The US Federal Reserve kept Fed Funds Rate unchanged at 3.5 to 3.75%, as widely expected by investors.

This follows its stance of maintaining rates unchanged in the January meeting, after cutting interest rates by three times in 2025.

More importantly, Fed Chairman Jerome Powell sent a caution message on inflation expectations. The Fed now expects personal consumption expenditures (PCE) inflation to be 2.7% in 2026, higher than the earlier estimate of 2.4%.

Core inflation, which excludes food and energy, is also expected to be 2.7%, up from 2.5%. Inflation is now expected to come down more slowly, with projections for it to reach 2.2% in 2027 and return to the Fed’s 2% target by 2028.

The Federal Reserve has signalled a more cautious path for rate cuts in 2026.

The dot plot, which shows the projections of Fed officials, indicates that most officials expect rates in 2026 to be between 3.25% and 3.50%, implying potentially one rate cut this year. While the median has not changed, some officials are now expecting fewer numbers of cuts. Four or five officials went from expecting two rates cuts in 2026 to expecting just one rate cut.

Similarly, Bank of England held interest rates unchanged at the meeting on 19 March 2026, compared to the earlier expectation of one rate cut. Policy makers also warned of rising inflation and slowdown in economic growth caused by the oil shock.

The Fed’s more cautious tone has pushed US government bond yields higher, with the 10-year yield rising above 4% and reaching about 4.34% by 23 March 2026.

When returns on safer investments like government bonds increase, S-REITs tend to look less attractive in comparison.

To stay competitive, REITs would need to offer higher yields, which usually happens when their prices fall.

In Singapore, the 10-year government bond yield has risen by about 33 bps month-to-date to 2.29%, as at 26 March 2026.

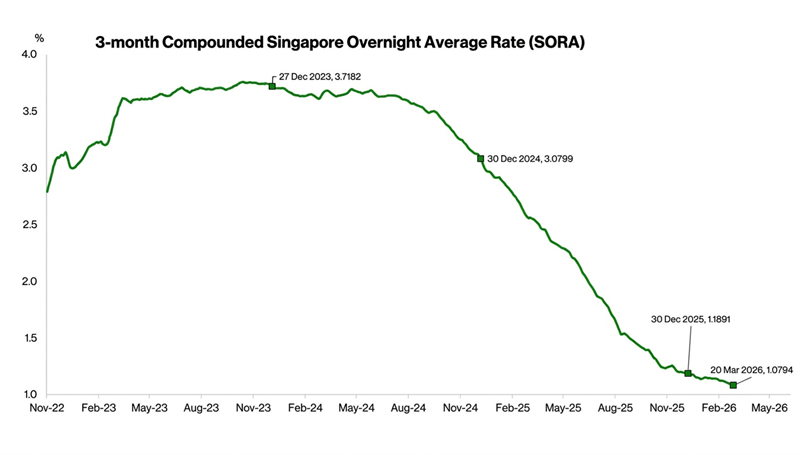

#3 – Funding cost may rise again

In 2025, S-REITs benefited from the sharp decline in 3-month SORA, the benchmark rate used for much of their borrowing.

As the Fed began cutting rates in late 2024, 3-month SORA fell to around 200 bps in 2025. This helped lower interest expenses, supporting higher distributable income and distributions.

Looking ahead, the outlook may become less favourable if interest rates move higher again. If inflation remains elevated, central banks may keep rates higher for longer or even raise them further.

In such a scenario, S-REITs could face higher refinancing costs over time.

Does the current pullback in REIT prices offer an attractive entry point?

With uncertainty around interest rates, the near-term outlook for S-REITs may be more challenging, and a broad recovery across the sector is less likely. Investors may need to be more selective.

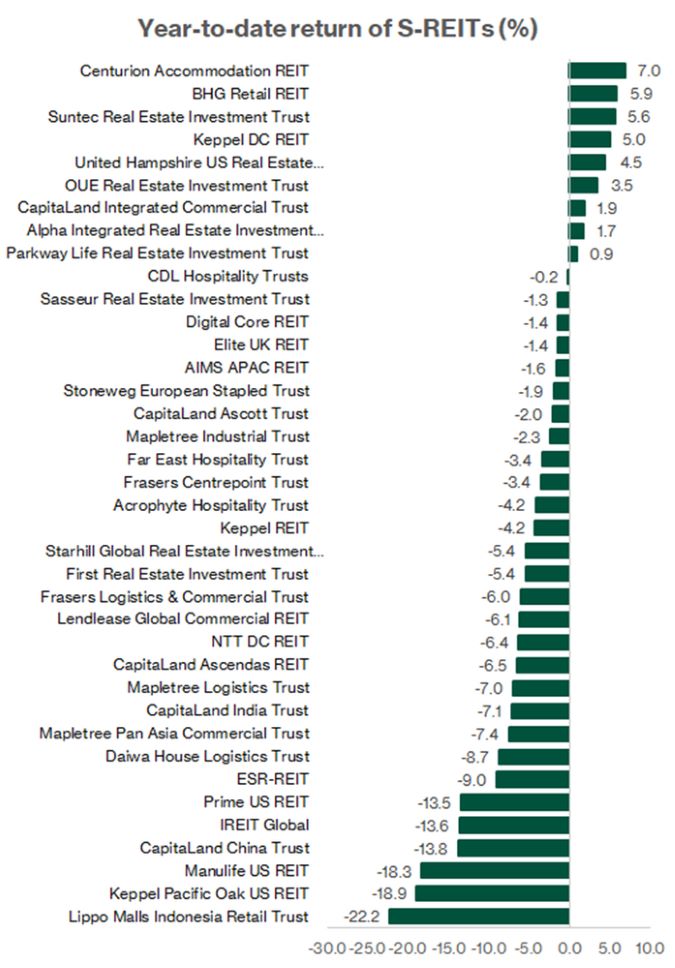

As shown in the chart below, there has been a significant divergence in the year-to-date performance of Singapore REITs.

In this environment, REITs with stronger assets and more stable demand may hold up better. This includes those focused on Singapore office, logistics, data centres and purpose-built accommodation.

Investors may also want to look for REITs that can maintain or grow their distributions through actions such as improving existing properties, making acquisitions or achieving higher rents.

Returns are likely to vary depending on the type of assets they own, where they operate, how their debt is structured and how well management executes.

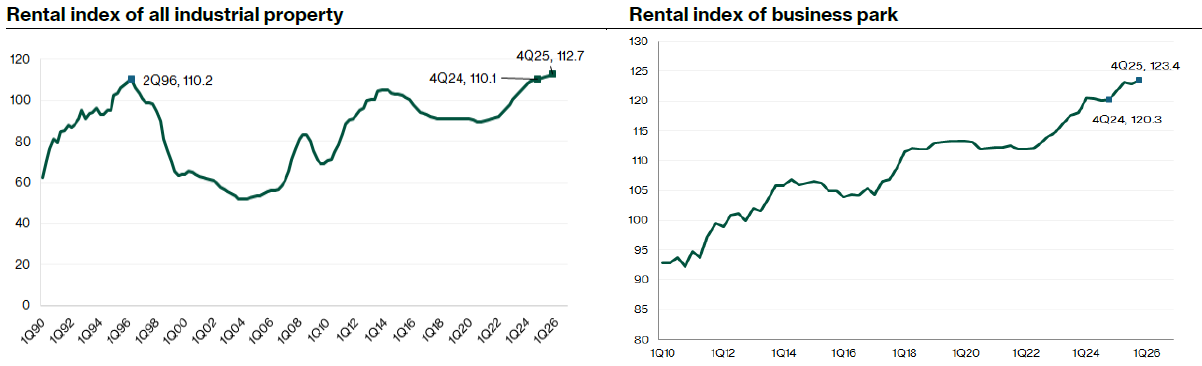

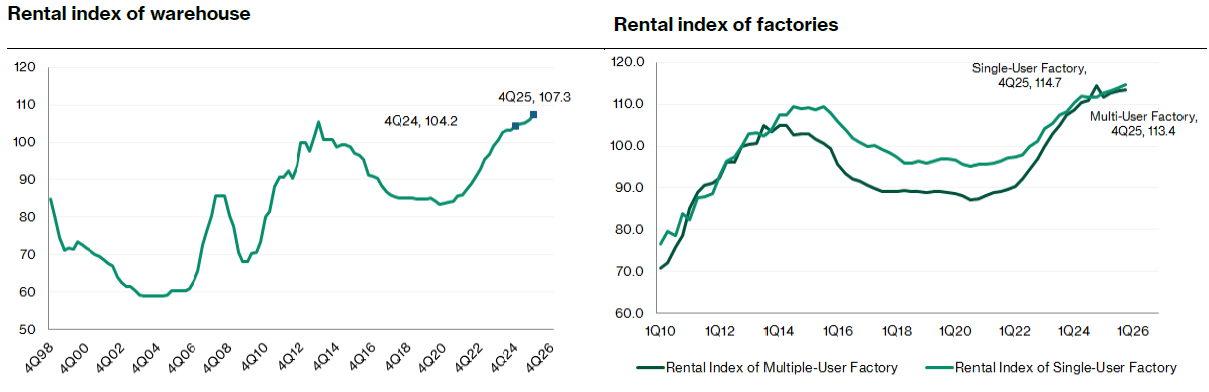

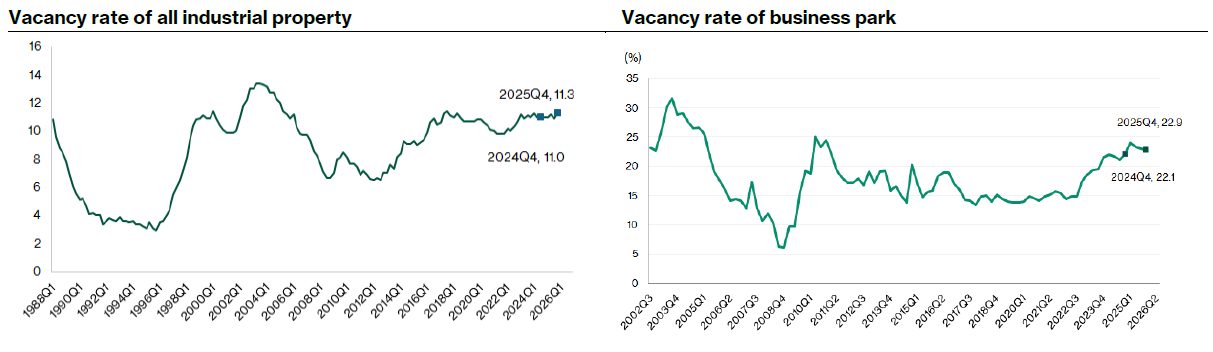

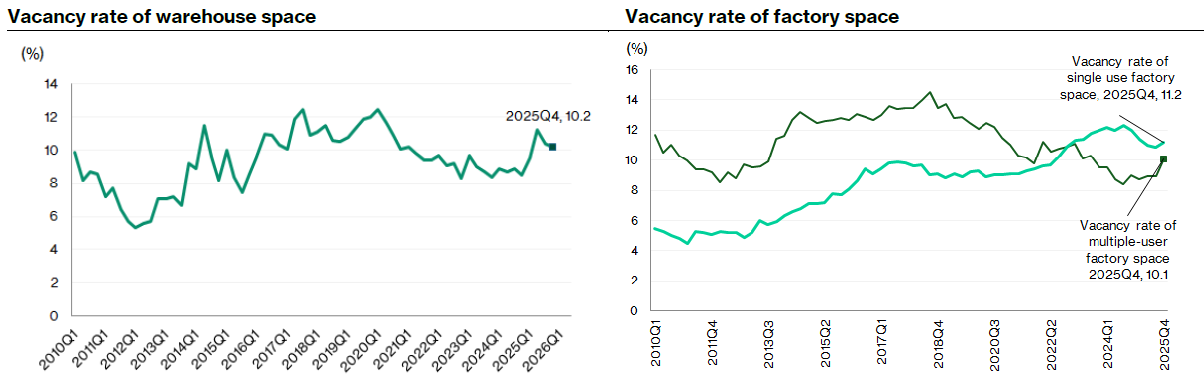

Fundamentals of selective sectors remain resilient as of 4Q25

Based on the key operating metrics as of end-4Q 2025, we believe the fundamentals of selective sectors remain resilient.

Singapore REITs reported 4Q25 results, extending the trend of higher year-on-year distribution per unit (DPU) led by lower interest costs.

Capitaland Integrated Commercial Trust issued long-tenor notes at 2.25%, well below its average cost of debt of 3.3% in 3Q2025. The interest savings flow directly into the distribution to unitholders. Capitaland Integrated Commercial Trust reported FY2025 distributable income increased by 14.4% year-on-year as cost of debt declined to 3.2%, from 3.6% in FY2024. Interest expense fell 8.9% year-on-year to S$314.7 million.

Keppel DC REIT’s average cost of debt fell to 2.8% in 4Q2025, from 2.9% in 3Q25. CapitaLand Ascendas REIT maintained an average debt cost of 3.5% in FY2025, down from 3.7% in FY2024. These developments signalled that the debt market was strongly supportive of REIT refinancing and growth.