What happened?

Singapore REITs dipped in March 2026.

With sentiment turning more cautious, many in the Beansprout community have been asking whether this has created opportunities among Singapore REITs again.

We recently looked at Singapore blue chip stocks that offer dividend yields of above 5%. In particular, Singapore banks now also offer more attractive dividend yields, with DBS’ dividend yield at close to 6%.

This led me to wonder if there are Singapore REITs that also offer dividend yields of above 6% with the pullback.

In this article, we look whether the dividend yields of these REITs are sustainable, and what investors should watch before adding them to their portfolio for income.

3 Singapore REITs with dividend yields above 6% after March pullback

#1 – Mapletree Industrial Trust (SGX: ME8U)

Mapletree Industrial Trust is one of the larger industrial REITs in Singapore, with a portfolio spanning industrial properties in Singapore as well as data centre exposure in North America and Japan.

As at 31 December 2025, Mapletree Industrial Trust had total assets under management of S$8.5 billion across 79 properties in Singapore, 55 properties in North America, including 13 data centres held through a joint venture, and two properties in Japan.

This gives Mapletree Industrial Trust a different earnings profile from a purely Singapore-focused industrial REIT.

While its Singapore and Japan assets have continued to provide a relatively stable base, its North American portfolio has become a more important swing factor for distributions due to lease renewals, occupancy trends and US dollar movements.

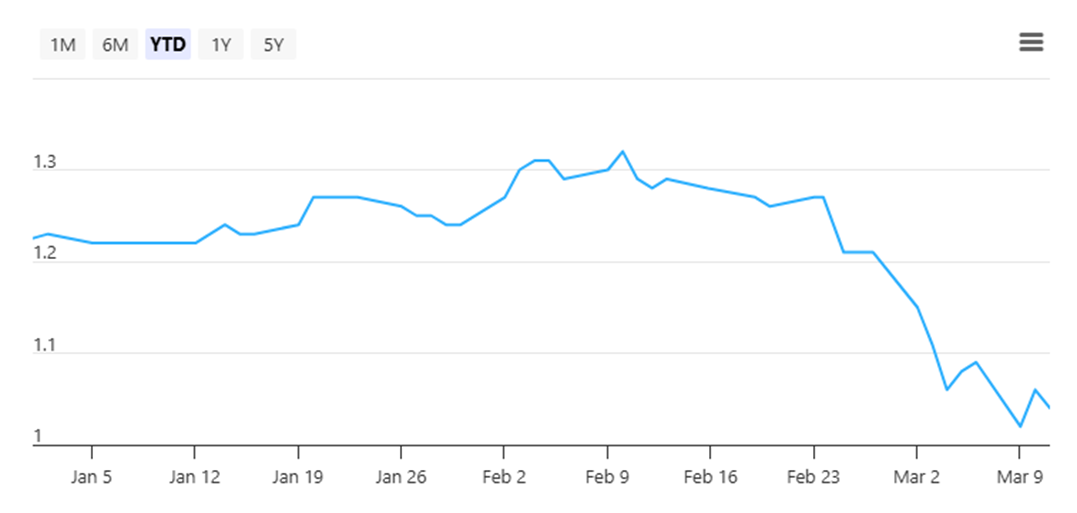

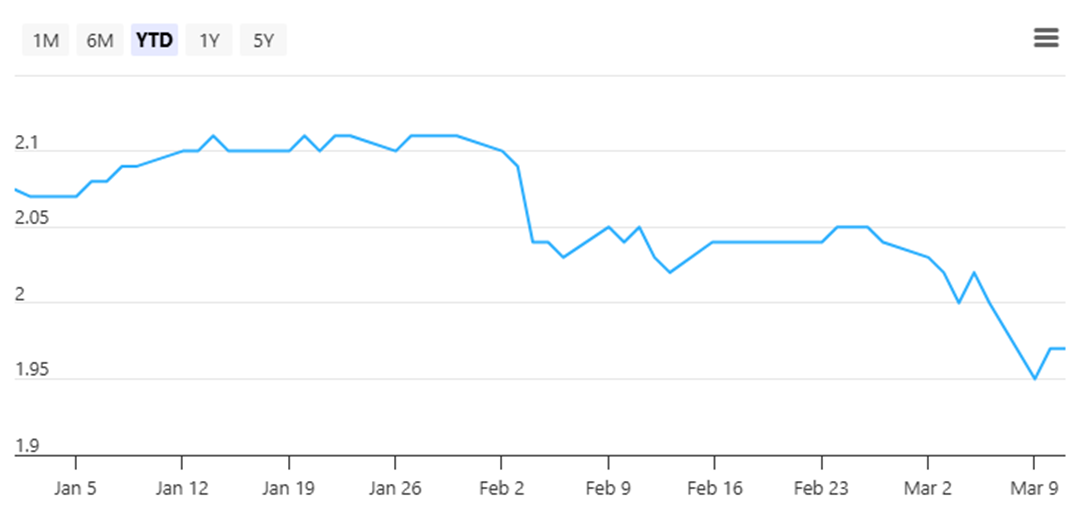

Following the recent sell-down, Mapletree Industrial Trust’s share price fell to S$1.96 as of 12 March 2026, leaving it down about 5.3% year-to-date.

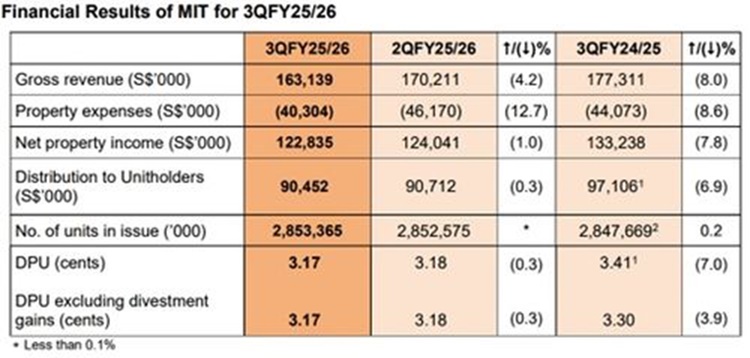

In 3Q FY25/26, Mapletree Industrial Trust reported gross revenue of S$163.1 million and net property income of S$122.8 million, down 8.0% and 7.8% year-on-year respectively.

The weaker performance was mainly due to the absence of income from the divestment of three Singapore industrial properties in August 2025, lower contribution from the North American portfolio following lease non-renewals, and the depreciation of the US dollar against the Singapore dollar.

These were partly offset by contributions from the Tokyo mixed-use facility acquired in October 2024 and the completion of the final phase of fitting-out works at the Osaka data centre in May 2025.

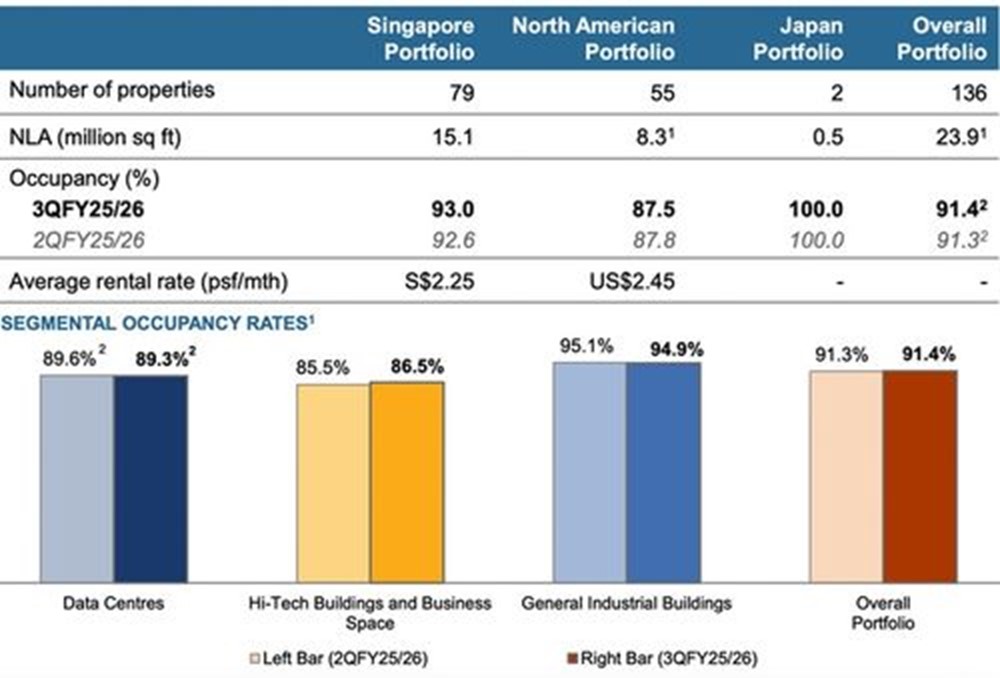

Operationally, average overall portfolio occupancy in 3Q FY25/26 was 91.4%, slightly higher than 91.3% in the previous quarter.

In Singapore, portfolio occupancy improved to 93.0%, while renewal leases in Singapore recorded a weighted average rental reversion of 7.1%, with positive reversions across both hi-tech/business space and general industrial assets.

MINT also saw a modest improvement in committed occupancy at Mapletree Hi-Tech Park @ Kallang Way, which rose 0.7 percentage points quarter-on-quarter to 65.1%.

In North America, the picture remains more mixed.

Occupancy slipped 0.3 percentage points quarter-on-quarter to 87.5%, weighed down by the non-renewal of a lease at 400 Holger Way in San Jose.

Even so, MINT continued to make leasing progress. It executed leases covering 217,062 square feet, or 3.0% of net lettable area, at a weighted average rental reversion of 3.1%.

It also secured a 13-year lease for a new tenant at the previously vacant 2055 East Technology Circle in Tempe, Arizona, helping to maintain the North America portfolio’s weighted average lease expiry at 6.2 years.

Management is prioritising longer leases to improve income visibility even as the portfolio works through near-term vacancies.

Another drag came from its second data centre joint venture. Cash distribution from the 50%-owned Mapletree Rosewood Data Centre Trust declined 14.6% year-on-year in 3Q FY25/26 due to the repricing of matured interest rate swaps, which resulted in higher borrowing costs.

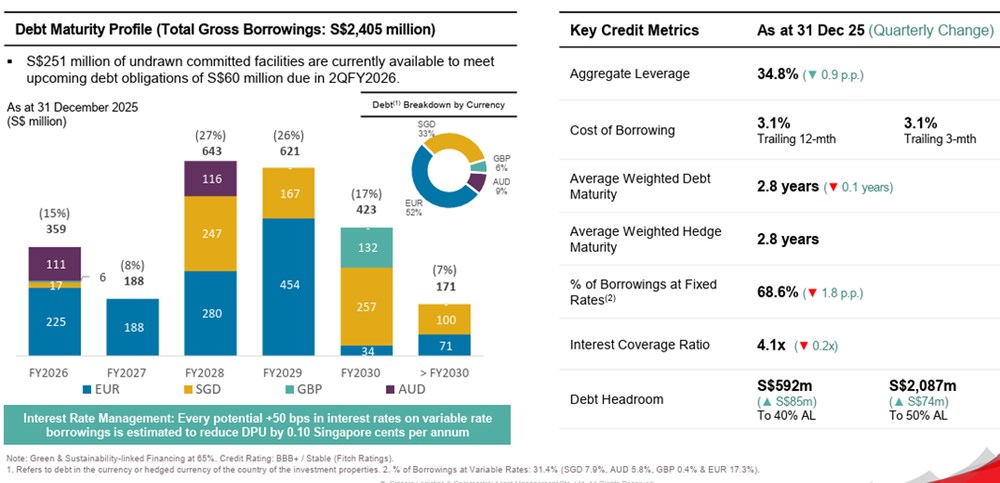

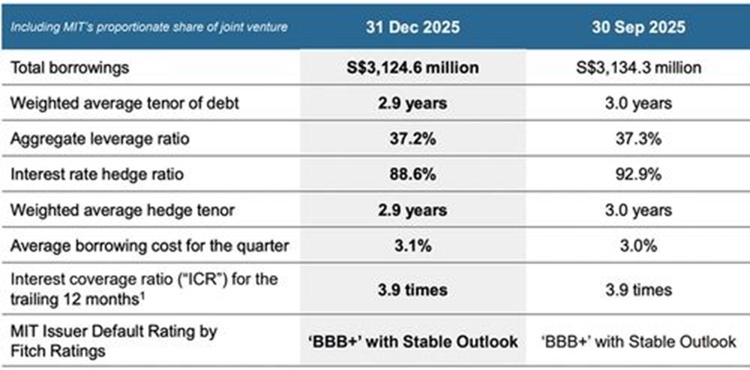

Mapletree Industrial Trust reported aggregate leverage of 37.2% and an interest coverage ratio of 3.9 times as at 31 December 2025.

The average borrowing cost for 3Q FY25/26 rose to 3.1%, and management noted that borrowing costs may continue to increase as earlier interest rate swaps mature and are repriced at higher prevailing rates.

It has guided for borrowing costs of around 3.1% to 3.2% for FY26 and 3.3% to 3.4% for FY27, which could continue to weigh on distributions.

That said, about 91.4% of the amount available for distribution over the next 12 months is either denominated in Singapore dollars or hedged into Singapore dollars, which helps reduce currency volatility.

Looking ahead, management remains focused on improving occupancy in North America, while pursuing selective divestments in North America and Singapore to improve financial flexibility and redeploy capital into assets that can support more sustainable growth.

In particular, Mapletree Industrial Trust is still targeting S$500 million to S$600 million of divestments in North America over the next two years, with S$100 million to S$200 million planned for FY26 and S$400 million to S$500 million for FY27.

The assets earmarked for sale are mainly data centres that are currently vacant or have smaller power capacity, and are therefore seen as more vulnerable to non-renewal risk.

Over time, this could help rebalance the portfolio towards higher-growth data centre assets in Asia Pacific and Europe.

Mapletree Industrial Trust announced a DPU of 3.17 cents for 3Q FY25/26, down 7.0% from 3.41 cents in the previous year.

This is due to non renewal leases in the US and downtime in North American data centers despite strong rental reversions in the Singapore portfolio.

Based on its unit price of S$1.96 as of 12 March 2026, and consensus DPU estimate of S$0.128 for FY26, Mapletree Industrial Trust offers a forward dividend yield of approximately 6.5%.

Find out how much dividends you would have received as a shareholder of Mapletree Industrial Trust in the past 12 months with the calculator below.

Related links:

#2 – Frasers Logistics & Commercial Trust (SGX: BUOU)

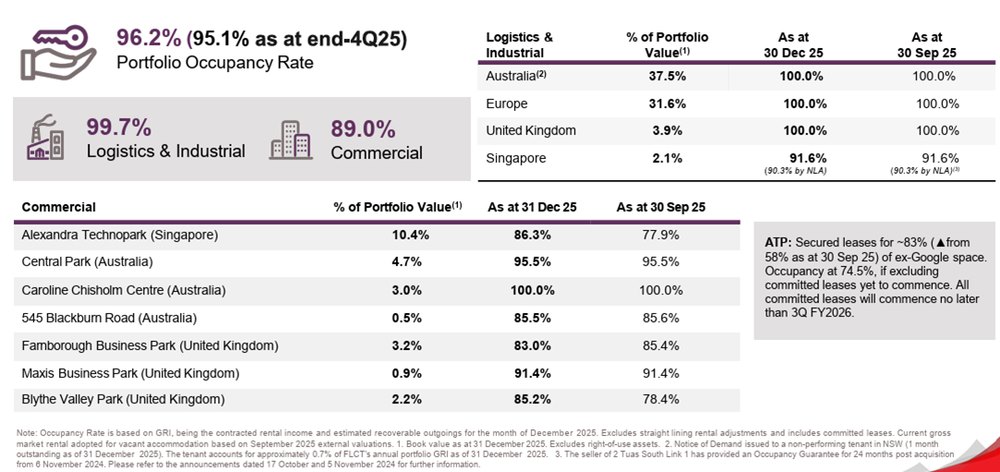

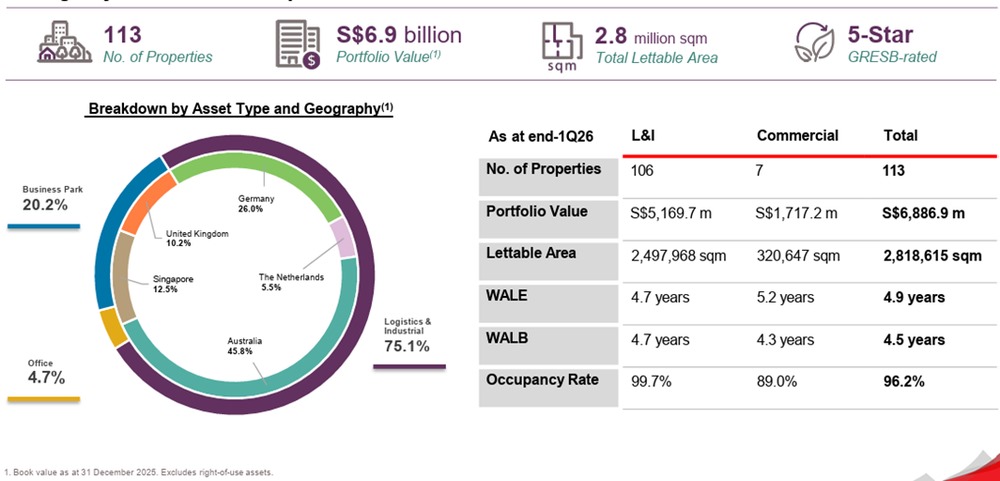

Frasers Logistics & Commercial Trust owns a diversified portfolio of logistics, industrial and commercial properties across five developed markets, namely Australia, Germany, the Netherlands, Singapore and the United Kingdom.

As at 31 December 2025, the portfolio comprised 113 properties with a total portfolio value of S$6.9 billion, with logistics and industrial assets making up 75.1% of the portfolio by value.

This gives Frasers Logistics & Commercial Trust a different earnings profile from a pure Singapore REIT. Its income is supported by diversification across multiple developed markets, but performance is also shaped by leasing conditions across different geographies and sectors.