What’s different about landlords in Singapore, compared to many different countries? The answer, to me, is the degree of tolerance they have for vacancies. Now this definitely isn’t true for every landlord, and it’s anecdotal; but I meet more landlords here who are willing to let a unit go vacant for as long as a year, rather than accept a lower rental rate.

That’s partly why Singapore’s rental market can feel oddly “sticky.” Even when the market sentiment weakens, rents don’t necessarily fall very quickly. This is partly due to the strict financing limitations we have, which tend to ensure property buyers are well capitalised: a maximum loan quantum of 75% (of price or value, whichever is lower), the Total Debt Servicing Ratio (TDSR), and so on.

Alternatively, as one of our readers so bluntly told me once: “If you’re rich enough to have a second property in Singapore, you’re rich enough to keep it vacant.”

Most of our landlords are unshakeable with what they consider fair rent; and if you’ve ever been a tenant, you’ll realise how quickly that reality sets in. Most tenants in Singapore are foreigners, who probably aren’t in a position to buy due to the high prices and 60% ABSD. Even if they’re worried about their career prospects due to AI, geopolitics, etc., they really don’t have much of a choice.

As for Singaporeans waiting on their next home, or who are unable to get a flat yet, they’re often caught in a similarly awkward position.

Delays in construction, divorce proceedings, children’s school arrangements, or simply timing the sale and purchase of homes can all force them into signing a particular lease. Quite often, they don’t have the luxury of time to look around for something more optimal.

This may explain some of the contradictions in Savills’ latest Q1 2026 rental report.

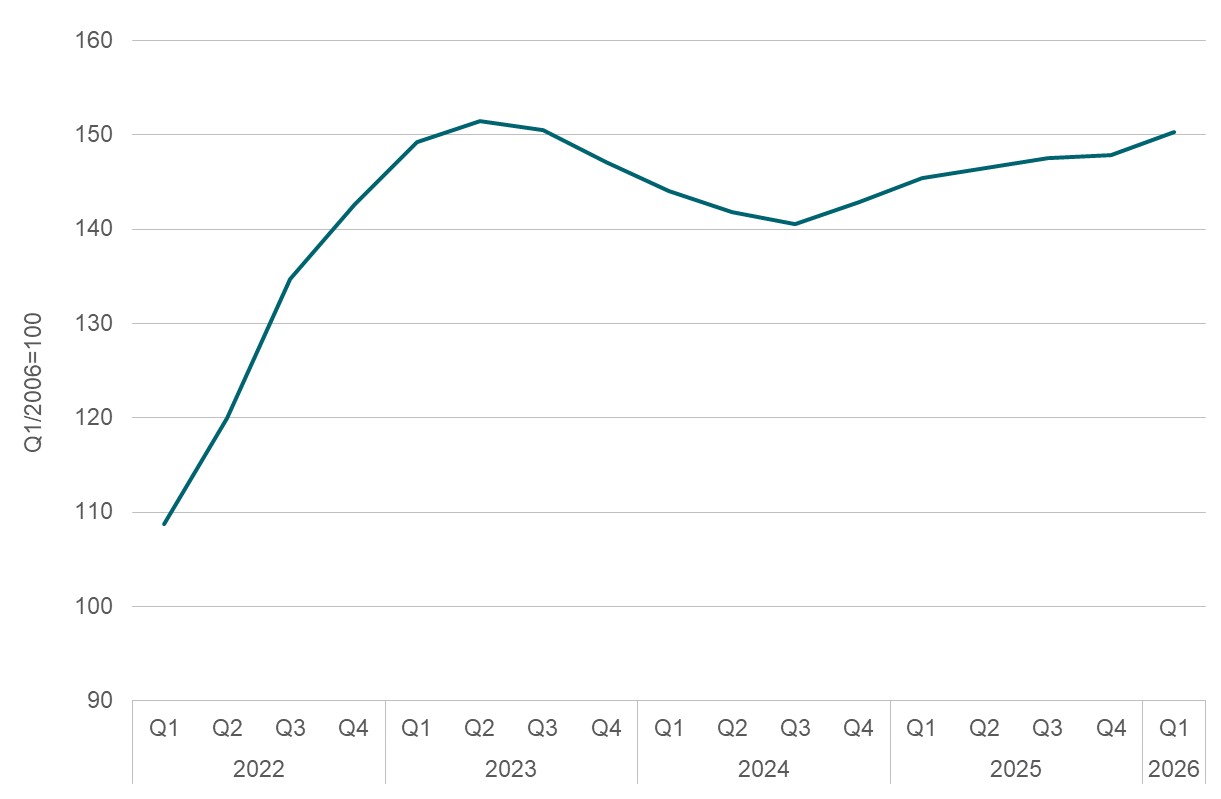

On paper, leasing activity actually increased in Q1 of this year: residential leasing transactions rose 4% quarter-on-quarter to 20,862 deals.

How much shorter? We don’t have the information. But here’s the thing: a higher volume of shorter leases doesn’t always mean strong demand. Instead, it could simply reflect more frequent renewals and renegotiations.

For example, a tenant may previously have signed a two-year lease because they felt assured of stable employment, or expected to remain in Singapore for the foreseeable future. That would naturally result in fewer lease transactions over time.

But if the same tenant is now opting for multiple shorter leases instead, leasing “activity” rises, even though the actual level of housing demand may not have changed very much. In fact, it could suggest the opposite: greater uncertainty about whether they’ll remain here long-term.

It may also suggest tenants are deliberately keeping their options open. If the rental market softens later, or if economic conditions worsen, they don’t want to be locked into today’s higher rental rates for an extended period.

So the increase in leasing transactions may not necessarily reflect confidence. It may instead reflect caution, flexibility, and a growing reluctance to commit long-term.

This also lines up with the broader market behaviour Savills described.

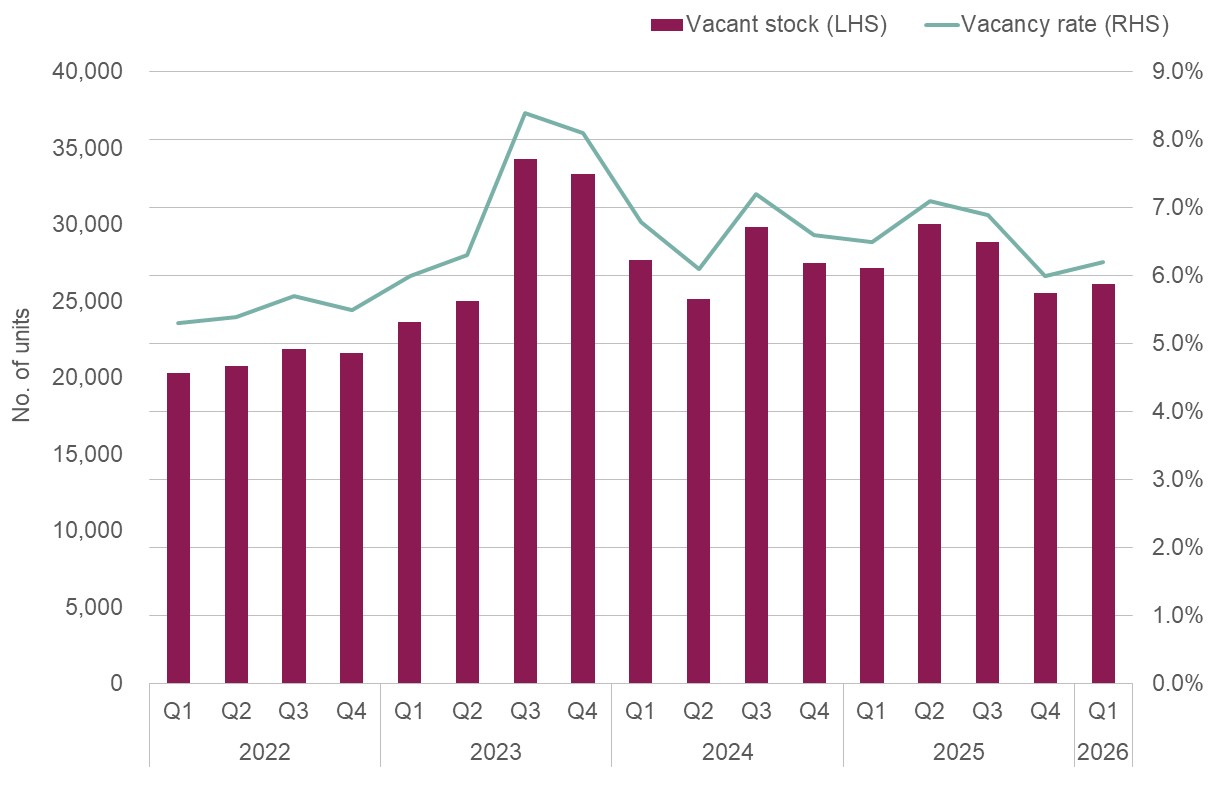

Whilst leasing transactions increased, vacancy rates outside the CCR edged upward.

Vacancy rates in the RCR rose to 6.3%, whilst OCR vacancy rates increased to 5.2%. Only the CCR saw improvement, with vacancy dipping slightly to 8.2%.

Now if rental demand were truly surging, we’d expect vacancy rates to fall dramatically across all the regions. Instead, all we see is a slight reduction in vacancy in the CCR, whilst vacancies in the OCR and RCR actually increased.

Read Full Article At Source